This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I started in 2007 with a thesis that my primary investment decision would be about the team (70%) and only afterward about the market opportunity (30%). But they are also a tax on your time with portfolio companies, looking for new investments, running your shop and honestly they are a tax on your family life. I don’t.

Everybody has a blog these days and there is much advice to be had. Many startups now go through accelerators and have mentors passing through each day with advice – usually it’s conflicting. Because I’ve asked more than 100 VCs similar questions I start to notice patterns in thinking. What is a founder to do?

I'm often the last one to leave an event, held back by the most persistant of entrepreneurs trying to squeeze as much advice as they can out of me. I've only recently started leading investments a little over two years ago. Often times, the advice is terrible or impractical. I mean, what do I know? It doesn't stop anyone else.

In normal times investors will look for “traction&# before investing. I spoke about this more in depth in these two posts: 4 things I look for in an investment & how to manage VC relationships. I didn’t invest in Orgoo but by the time he launched Ad.ly This is happening with both angels and VCs.

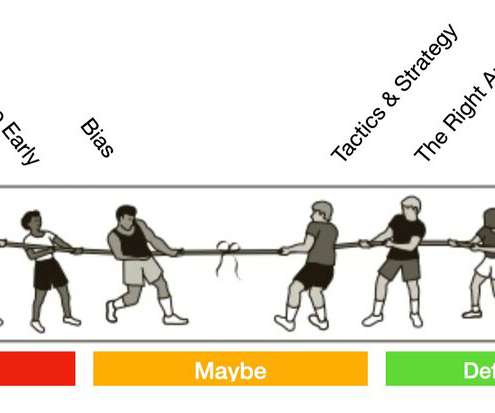

The startup ecosystem is a terrific manufacturer of bad fundraising advice. Any VC will tell you that the ones they said yes to, they mostly got there right away—and that there are very few “maybe” deals that get tipped over the fence. Was she just an anomaly or is there something else going on here? First is network bias.

Picking a VC is hard. So I thought I’d write about out with what I would look for in a VC knowing what I know now and why. Most VCs are book smart. VCs should be more of a coach than proscriptively telling you what to do. You want a VC who will spar with you but then STFU and let you get on with things.

I always get asked how to get into VC and so I think a lot about what it takes to do the job well. I'm way early in my career, so I won't say I've perfected anything yet, but after 8 years on the investing side and 3 in startups, I've come up at least one thing: Be open. For a VC, I think the process of raising money humbles you.

What is a principal at a VC firm and how does it work at Upfront Ventures? ” Associates have different functions at different VCs. VC firm admin. VC firm policy or fund analysis. Helping be the VC “presence” at key events. inside insight into VC decision-making. Industry reviews.

It spoke to me because it so resonates with my nearly daily advice to entrepreneurs and VCs alike. I went as far as to call it the best Tweet of 2015 so far because it encapsulated my advice so succinctly. I am often asked how we make decisions on investments at Upfront Ventures. He took two words where I take 1,000!

For some aspiring to be tech entrepreneurs, I often suggest a two-step process, as I argued in this post that “ The First Startup Founder You Need to Invest in Is You.” But I also have advice for the 15% that really do want to be a startup CEO. I often tell people in this scenario to focus on a VC “fixer upper.”

I can't tell you how many times even insiders--people already invested in some of these companies--are telling diverse founders to go for incremental fundraises and not for bigger rounds. So if you're a super early stage with just a prototype, you might not think that a VC fund is the right fit for you--so you wind up at an angel group.

We have been advising a lot of entrepreneurs so I thought I’d “open source” some of the advice I have been sharing. But I have been in close contact with the NVCA, many of the major law firms and many of the major VC firms. Am I ineligible since I’m VC-backed? I am not claiming to be the world expert on this. shouldn’t I?

And I am often approached by entrepreneurs in cities which don’t have a vibrant VC community. If you don’t live in a major VC zone, I have some tips for how to make it easier to raise Venture Capital. ” Most VCs view it as their responsibility to mentor, debate, cajole and generally assist with investments they make.

I spent countless hours with VC firms, startups & LPs (the people who invest in VC firms). On my first real day back the first thought I have is that most entrepreneurs don’t manage their VC relationships as well as they could. It’s best to think of your VC partnership as a customer.

VC firms see thousands of deals and have a refined sense of how the market is valuing deals because they get price signals across all of these deals. It’s not uncommon for a VC to ask you how much capital you’ve raised and what the post-money valuation was on your last round. So why does a VC ask you?

As a VC you want to feel like you have “proprietary sources” of deal flow. There is one source that was always problematic for me – intros from investment bankers. This is no criticism of the investment banking industry (although I’m sure some will read it this way) for which there are very useful purposes.

Most conversations don't end in funding or even a follow up meeting, so your aim should be to get specific, helpful advice that moves you forward. He realized that rushed in person pitches don't do your company justice at all--especially when VCs are running to another meeting or trying to mingle and meet as many people as possible.

Why do VC's get such a bad rap? That's literally your baby--and 98% of the time, a VC will tell you that your baby is ugly. We're "kingmakers" whose investment has the "Midas Touch." That's probably why the vast majority of applications for VC positions tend to be from males. So what gives? 3) Access to money.

This is part of a series of advice for founders who need to raise money from venture capitalists. The most important advice I could give you before you set out in fund raising mode is to understand that fund-raising a sales & marketing process and needs to be managed. an investment in your company.

I just want to figure out what a fair valuation is.&# I figured all the VC’s talked so we should. How VC’s Calculate Valuation : We walked through a standard deal where you raise $1 million at a $3 million pre-money valuation leading to a $4 million post money valuation. The VC assumes you’ll have an option pool.

As a VC with scores of startups in our portfolio we have ringside seats to many, many fund raising processes plus I had to raise money across about 5 different rounds of capital as an entrepreneur so I’ve developed some thought on the process that I hope can be helpful to some of you before you start. Just send me your dog damn deck 7.

As a VC and former entrepreneur let me offer you some advice. Remember that the goal of an email to a VC or an introduction from a trusted mutual connection is simply to get you the meeting. Remember that the goal of an email to a VC or an introduction from a trusted mutual connection is simply to get you the meeting.

But less as a complaint and more as advice to younger networkers, the more you invest in relationships the more you will get when you need. ” In it he talked about how he gets daily emails asking for intros to Oprah (he does a lot of work with her) and his advice. “I’ve never been a VC before.

I only say that because after years as a VC I can always tell when my peer group invested in something because “it seemed like it would make money” versus when they invested out of passion. On reflection of the role that I want to play as a VC it is clearly in the camp of passion. I’m a VC.

I became a VC 12 years ago in 2007 when the pace of deals was much slower. As I was trying to figure out the role I wanted to play in the VC world I decided I wanted to focus on businesses that were building deeply technical products to solve problems for business users. We not only have our Series A funds that can write $500k?—?$15

If you are a super young, well-connected, Stanford CS or EE, worked at Facebook early, have a bit o’ dosh and have VCs chasing you … you are exempt. My VC told me that if we monetize too early we will scare away our nascent marketplace and not grow as fast. If that’s you, you can ignore my advice.

It’s the first EIR that we’ve had in the years that I’ve been with the firm and I hope will be the start of our investment in this program. We’re excited to continue to grow our investment professional staff and will continue to do so over the course of 2013 & 2014 with our new fund.

In the VC insider baseball world a discussion has gone on about “VC platforms” over the past 5 or so years. While firms define platforms differently, let’s just say they are the services that a VC offers outside of investment capital and partner time on boards or providing intros.

It got me thinking about the advice that I often give to new VCs. For years I saw myself as the new guy in VC but then you wake up one day and realize that 50% of your peers have been doing it for less time than you and time has moved on. VC Industry' It’s exhausting. Perhaps unsustainable. Lines, Not Dots.

” I found myself nodding through all of it with quotes like, “Seed investing is the status symbol of Silicon Valley,” said Sam Altman. They now have a strong VC lead from Foundry Group and from experience when you get advice from Foundry it comes with authority, experience, empathy and the right amount of straight talk.

If you’ve been following the press about VC funds you’ll know this is no small feat. VC has operated as an “old boys club”, with access to capital often requiring entrance through an elite university engineering department in one of two cities. Startup Advice' See what we did there?

If you’re an entrepreneur who would like to see this clause in more startups please ask your VC to include it in future term sheets and link to it from their home page. “We We strive to invest in companies that are consciously working to create a diverse leadership team?—?one Ours is: upfront.com/inclusion. It takes a village.

You can watch the video above for a very brief overview of why we rebranded and where we see our place in the VC ecosystem along with what has changed in our industry. Relaunching our brand is part of our larger initiative to build a VC firm of the future. Startup Advice' Nearly four months ago we rebranded at Upfront Ventures.

Ok, back to the VC content marketing. As a result I’ve seen hundreds of VC decks, all certain they will be among the top performers. Most strategies are some combination of innovation and best practices along the classic five steps of venture investing: See, Pick, Win, Service, Exit. This post is about ‘seeing.’

By spending more time educating your board on your business you get more valuable advice from them. Your goal should be to turn your VCs into extended members of your team to get real value from them. Each of your angels or seed investors may have 20-30 investments. Ask your VC to send a critical email to a contact.

I am a VC. But through expressing points-of-view I can raise above the consciousness of my customers (entrepreneurs and limited partners who invest in VC funds) in ways that I couldn’t without breaking through the noise of the hundreds of others of VCs who also have money. I hand out money.

I rarely talk to any startup entrepreneur or VC who doesn’t feel it and somehow long for simpler times despite the benefits we all enjoy from increased enthusiasm for our sector. There are too many pulls & tugs at our elbows for time, for coffee meetings, for advice or speaking engagements or cocktail parties or dinners.

Because my role as a VC requires me to take and endless stream of meetings I long ago decided I need to learn as much as I can from the meetings I attend so I often just ask tons of questions and assimilate knowledge. When I think about what defines us as a VC I think: Operationally knowledgeable / strong startup competence.

I've seen this so many times over: A founder pitches a VC, or several of them, and then they come back from that process with all sorts of new strategy goals or worries that they need to be doing something differently. They don't want to invest in your company. Any advice they have for you is going to be a bit broken.

I got three calls from another big name, big check VC. For all the things he’s likely known for, he probably hasn’t yet built a strong relationship as an early stage venture investor (he invests often in later-stage deals where he is very respected). Why am I so lucky? I looked at all three deals. I’m not sucker.

This is largely driven by large investment flows from strategic and tourist investors. VC firms are not blameless — over 1.8K VC investors wrote checks into proptech deals over the last five years. Strategics in this space typically have a portfolio of hard assets (i.e.,

As a VC you want to feel like you have “proprietary sources” of deal flow. There is one source I never liked and no early-stage VC should – investment bankers. This is no criticism of the investment banking industry (although I’m sure some will read it this way) for which there are very useful purposes.

You’re not a master of what’s on the menu and you don’t want to invest the time to parse through all of its complexities. Don’t build for yourself or your friends who use your product and say, “wouldn’t it be nice if you could just …” And certainly don’t build for your VC.

I had dinner this week with a top new customer at one of our enterprise software investments. I wish I did more enterprise software investing because when I attend meetings like this I realize that this is my core DNA – rolling out business software solutions to customers. Contrast that with a VC conversation I had.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content