Good morning! I am writing to you in the minutes before I have to pack up my writing and podcasting setups so that I can catch a few planes to San Francisco for Early Stage. (I’m moderating two sessions, including one on scaling ARR, so come hang!) My colleague and frequent collaborator Anna Heim wrote the real Exchange today and it’s a banger. Consider this some sort of bonus.

The SaaS selloff may be behind us.

Declines in the value of technology stocks have subsided, with public cloud companies appearing to have found a new trading level that they can somewhat comfortably hover around. This is at once good and bad news for technology companies more generally, and tech startups in particular.

It’s good that the rapid, kind of terrifying valuation declines we saw among modern software companies in the final months of 2021 and the opening months of 2022 have halted. And it’s somewhat unfortunate that the market repricing of the value of software appears ready to stick.

The Exchange explores startups, markets and money.

Read it every morning on TechCrunch+ or get The Exchange newsletter every Saturday.

More simply, the decline in the value of annual recurring revenue, or ARR, may be slowing, but there’s also scant indication that we’re about to see a rebound.

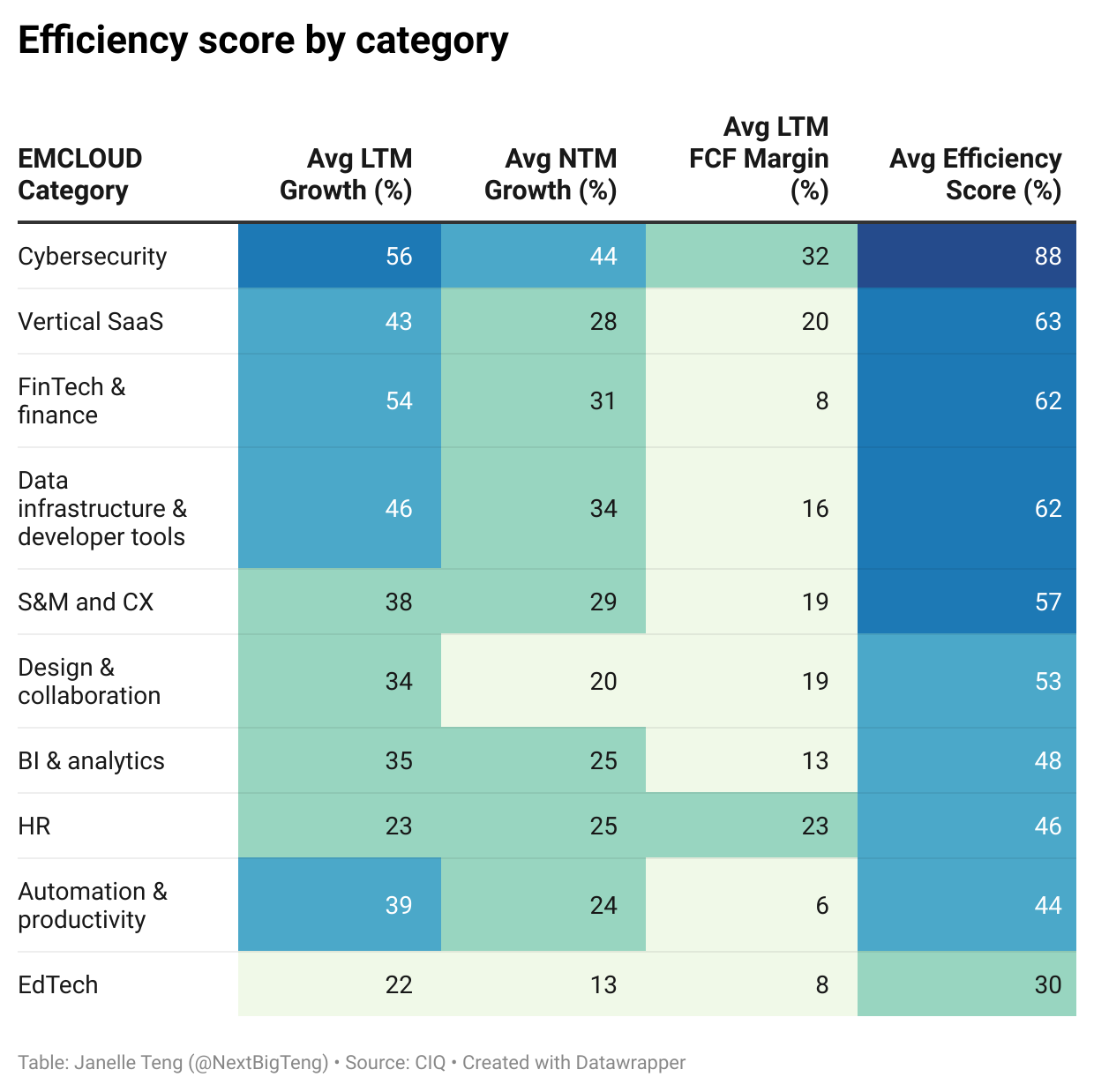

Bessemer’s Janelle Teng recently posted a useful analysis that digs into a few macro factors that have been pushing the value of tech stocks around. The key is the inverse relationship between interest rates and tech stocks: The higher interest rates go, the lower software stocks go, more or less. (The mechanics behind the dynamic are somewhat immaterial for our purposes today; it’s the relationship that matters.)

Ironically, interest rates may be the best reason to expect that most of the selloff in software stocks is behind us.

This may seem counterintuitive. Given that interest rates are set to rise in many geographies this year — and rapidly in the globally critical SaaS market of the United States — doesn’t that mean that more stock market declines are ahead? It’s a fair thought.

But markets price in expectations as well as results, and with inflation running hot in the United States besides the fact that we’re months into a general consensus that rates are going to rise sharply this year, we can expect that most of those bumps are already priced into software stocks.

The lumps have been taken, in other words, even if most of the actual rate bumps have yet to come.

Looking around, what is our new normal? Leaning on Teng’s number crunching, it appears that high-growth SaaS companies (greater than 30% growth) are worth around 14 times their next year’s revenue, in enterprise value terms today. Faster-growing software will be able to secure a greater multiple, naturally, but the number of SaaS or cloud companies on the public markets today that are trading for more than 20x their projected next-twelve-months (NTM) revenues is only six, per Bessemer data.

That means that nearly every single startup by the time they go public will be worth less — possibly a lot less — than 20x their next year’s revenue when they do go public. Pencil that into your valuation targets.

The good news is that the numbers might not get worse! The bad news is that I don’t see any reason for the new normal to become the recent past. The market has changed and software valuations have shifted. And if you enjoyed the free ride that SaaS valuations saw amid the pandemic, you can’t really get mad when more normal times replace an anomaly, right?

So what about edtech?

Ah yes. One more thing.

Teng’s analysis includes a breakdown of software company categories that compares average growth rates, free cash flow margins, and operating efficiency. In almost every category, edtech has the worst numbers of all cloud company cohorts. The only thing that edtech has going for it is slightly better free cash flow margins than “Automation & Productivity” companies. However, that modest beat in a single category does little to make edtech not an outlier in negative terms.

{kind=link}

Perhaps that’s why it took a pandemic and a global move to at-home school to ignite the category.