Next phase of #Fintech and #Insurtech is coming in 2017

Beginning of the year I blogged about the Outlook on #Fintech and #Insurtech in Europe here. I predicted a shift in this space for the first generation of fintech companies:

- A slim, focused B2C model needs to pivot or to be extended towards higher value products

- Customer gain via feature driven USP’s will become unsustainable because traditional players will catch up quickly and keep their incumbent advantage in the pure banking and insurance play.

- B2B tech players will be the winner in the first phase with highly profitable earnings. They will attract funding from VCs due to the scalability of their business models.

- B2C investments will have a hard time to convince financial industry experts of their success but will blend the public opinion with good PR and customer numbers. Many VC investors will try to save their initial investments with follow on bridging to win the survival game for now.

Watch out for the Trend

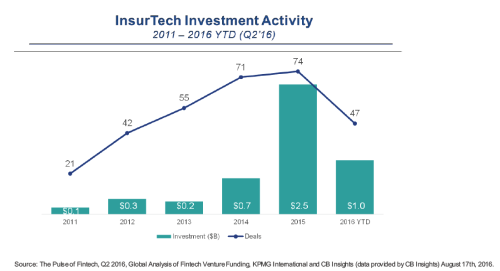

The investments in the Fintech space is still ongoing and keeping pace from the many seed investments in 2015/16. But as in all VC investments currently and in the first quarter of 2017 we see the drop in follow on investments for A-rounds and B-series. We are on a good track to reach the same level as last year which is in comparison a rather weak signal for now.

Investors across all stages have learned to select the better companies. So expect well educated VC partners when talking to them in fundraising. The first phase was the hot new thing as usual and everybody went for it. Now the first fingers are burned and rational thinking is back in the partners room when making investment decisions. Focus will shift to the more challenging topics and more industry driven. A horizontal approach is nice — but not winning the game if you are not the next Albert Einstein in tech. Platforms already taking over the horizontal spaces like mobile payment (Apple, Google, Alipay) and peer-to-peer payment (facebook, WeChat). Merchants will follow the customer’s money (Alipay, WeChat building on Chinese tourists abroad) and mass markets (Android and iOS devices). A simple P2P app will never reach critical mass to become significant nor will the business behind that become profitable anytime. Merchants also follow cost optimization so there is only one way to enter those product segments: do it for free! If a merchant doesn’t need to pay for an additional payment method he will eagerly try it out. No additional costs means: no fees and no additional hardware. So if you can do it with standard NFC terminals you can win a new merchant. Some banks already started their whitelabled apps being compatible with the NFC chips of Android handsets either smartphones or wearables/watches/fitness tracker.

Focus on industry segments but Mobile wins.

Deloitte published their view earlier this year and draw a picture of potential business models. There are more like this outside.

What all of those are missing is the impact of Mobile. Mobile will eat everything — because there is no difference between online and mobile. You get the same processor power, storage, speed and networks but all of this instantly and everywhere. Still the biggest game changer in this world and for all industries is Mobile.

T-Mobile US launched SynchUp with Mojio in November. First batch of products were sold out within days because customers liked the bundle of connectivity, pricing plan and feature set. There are a lot of those products and services out there in various regions. However only a few companies have the reach and customer base to build on to drive down customer acquisition costs and marketing spending. Partnering is always a good option for those B2C models — so becoming a B2B supplier wins markets which drive to commodity very fast. Without mobility in the core of the product it is hard to win a space. Connecting traditional services like car insurance with mobility and fast networks will allow to keep your margin and attack the competitors customer base on the move.

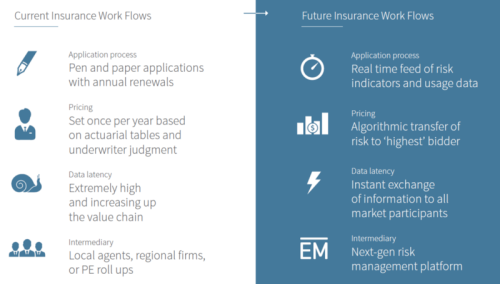

It’s all about Changing the Workflow

When disrupting an industry it is about changing the way we use a service. MyTaxi gained the market when it changed the way how people ordered a cab/taxi and paid for the ride all on the mobile phone visualizing every single step. A whole new experience of a service we know for over a hundred years.

“If you want to win in disruption change the way a customer uses your service and make it easier as well as more transparent. Technology in the background will create the new customer experience.”

This is true for Insurtech as well as Fintech:

Digg deep into the old traditional products and rethink the way a user in a mobile world will use it. Big Data analysis of every step and data, AI for all the steps and data a user will provide and Automation to create a higher flexibility will lead the way in successful products which new market leaders will grow from.

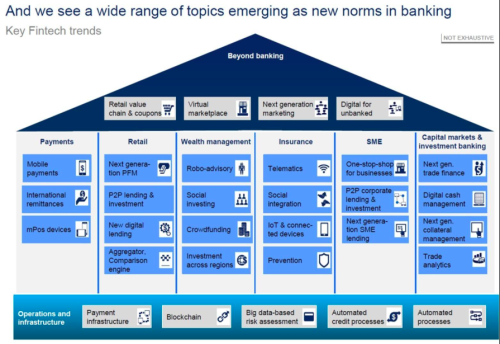

McKinsey’s view on the overall space gives some guidelines where to look for chances:

But be aware: Don’t underestimate the incumbents — They can buy technologies from B2B fintech and insurtech startups and build a piece by piece a much faster and stronger service platforms. There is no time for a shiny UI/UX if those can be build easily by others as well. As in every industry it comes down to price and value of a service from a customer’s perspective.

It needs to be a long term advantage — short term can easily be bought with deep pockets.