The Pre-IPO-Dip: The Opposite of the burst of a Dotcom-bubble

Many were talking over the last 12 months about the return if the dotcom area. The Bubble 2.0. A financial impact similar to Lehman and Quantative Easing. But to my estimation it will be the opposite of the events from early 2000’s.

However this isn’t good news. It will just be different and look nothing like everybody is expecting it to be.

So here is what will happen: Instead of public markets going down fast in a very short time like one and a half decade ago the private markets will implode, evaporate billions of investments and a multiple of that in valuations. The interesting thing about this is the group of people being impacted by this. From a quantitative perspective it will only hit a few people and firms compared to everybody who is active at the stock markets worldwide.

Only a limited number of investors are able to invest in private markets. That will limit the outcome of damage. The number of companies might be medium but the economical impact on revenues impacted is limited as well when taking the top 10 U.S. companies into account.

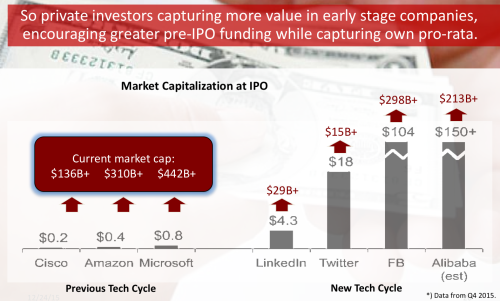

When looking on private markets we will see companies like uber, dropbox, square, snapchat etc impacted. Public companies like Apple, Amazon, Google and facebook are not impacted in their businesses. What will implode is the upside of private markets — not the value of public listed companies. Bare this diagram in mind: Public companies used to gain 100x on its IPO prize while today they will gain less than 10x on their IPO valuation.

Graph: Valuation uptake of public companies from late 1990’s compared to late 2000’s companies

We have lived through three phases in this Internet investment century

Dotcom Era: Companies moved to public markets rather soon hence the private market in the late 90’s were not able to offer the funds needed by Netscape and others for their expansion plans. IPO was the only way to get access to multi-million of cash to fuel the technology and hardware needed as well to hire the engineers who couldn’t be attracted by post IPO shares alone. There weren’t super sized VCs or PEs to invest billions into private companies during these days.

Unicorn Era: Facebook as a role model took as much funding as a private company as it was allowed by SEC and their regulations. Facebook was forced to go public due to the number of private investors it had so SEC demanded the same reporting rules as if it were a public company. Facebook took a short dip in its IPO valuation compared to its last private valuation but since then has more than doubled its valuation based on a revised mobile strategy.

Today: The end of the unicorn era is coming and private companies will be forced to go public again like in the Dotcom era to raise the needed funds for expansion. No private investors are willing to risk investments in private rounds until the IPO is close by. They are all waiting for the more increasing ‘Pre IPO Dip’ every private company has to take to make it till the public market.

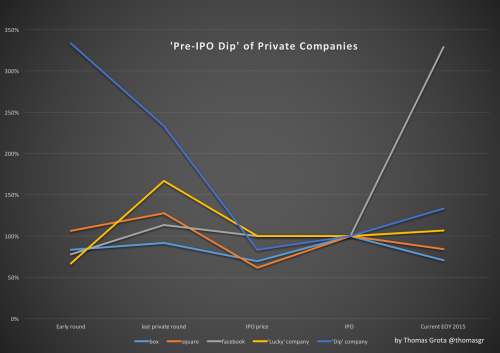

The “Pre IPO Dip”

Besides the option to reach breakeven private companies will need to go public for its final financing round. Public markets are not willing to pay unicorn valuations (20x valuation of revenues at 3x net loss multiples on those revenues). Private companies are forced to lower their valuations ahead of an IPO. This dip in the valuation curve is already visible in the latest IPOs of unicorns and will increase over the next year.

As soon as this strategy of “Pre IPO Dip” will become mainstream VCs and PEs will stop investing in unicorns in late stages and will wait for the last pre IPO round, which will be a down-round for most of the invested capital deployed to the company. This point in time be the most rewarding investment opportunity from a financial return perspective expressed in IRR (internal return rate):

- Short investment period

- maximum protection due to first stage liquidation preferences

- minimum risk due to most sophisticated due diligence in a pre IPO stage

The graph above shoes valuations of different companies for some stages of financing relative to their IPO market cap in percentage.

Who will suffer from this investment change?

Early stage investors from A rounds to C/D series will take the hardest hit on their investments. While seed investors have less invested capital in those deals and late stage investors are protected by liquidation preferences and full ratchet anti dilution protection the middle will be forced to take the losses in their expected multiples. Those companies used to raise high A series and continued to raise C/D rounds at billions valuation. As we have seen in Square’s IPO the IPO pricing came down to almost 50% of their last financing round and the current market capitalization is still far below the last private valuation.

Market capitalization of companies from early private rounds to current public market valuation

Private investors will take huge losses but no impact on public markets

During the burst of dotcom bubble in early 2001 a lot of public investors including ordinary people took the losses this time the private investors will be hit. Compared to the number of investors in public markets the number of private investors is very low. Only a fraction of overall investors with larger investment amounts will suffer those losses. It won’t be ordinary people who invested in some strange online businesses they didn’t have enough information about. Those are sophisticated professional investors, who made investment based on due diligence and insides of the companies they invested in. Public markets will be hit harder by decision of FED, ECB and Chinese regulators than what happens in the private investment markets. It won’t be another Lehman and nothing to be worried about for the everybody else.

Get prepared for a world without unicorns and back to normal investment rationals. Smaller companies with early focus on cashflow. Also be aware that the Internet giants will lead our daily life and fulfilling our daily needs. It is back to normal for everybody. A bit boring you might say. But boring can be good because it gives us time to focus on other important things like family and a walk in the park.