Rent the Runway is expected to price its IPO later today and trade tomorrow morning, provided that all things go as planned. Udemy is also on the way to the public markets. Allbirds, too.

And this week, Sweetgreen threw its hat into the ring.

Sweetgreen is a food chain best known for salads that are popular with the office-lunching crew. I can safely say that as a longtime member of that cohort back when I worked in an office in a major city.

Why are we talking about a fast-casual restaurant chain here on TechCrunch? Because Sweetgreen raised hundreds of millions of dollars during its life as a private company, including myriad venture capital rounds — through a Series I in 2019 — along with capital from other investors.

It’s an incredibly well-backed unicorn, in other words. It just happens to make salads instead of, say, enterprise software.

So, let’s take a dive into its IPO filing, working to both understand the company’s business and its results. We’ll close with notes on how we have no idea how to price the company, a similar issue that we had with Rent the Runway.

The following days and weeks are going to prove illustrative in terms of the value of tech-enabled businesses, especially in contrast to more digital and hard-tech efforts. Yet again.

The fast-casual food game

Sweetgreen operates its 140 food spots in 13 U.S. states and Washington, D.C., with some 1.35 million customers placing at least one order in the 90 days concluding September 26, 2021. And for a technology angle, some 68% of Sweetgreen revenue was generated from digital orders for its fiscal year to date, which ended September 26.

As noted above, office culture has proved to be no small part of Sweetgreen’s growth. Per the company’s S-1 filing, observe how it discusses the impact of COVID-19 — which disrupted going to offices, period — on its business (emphasis: TechCrunch):

We experienced a decline in our In-Store Channel due to the COVID-19 pandemic in fiscal year 2020, particularly in central business districts, which was partially offset by strong sales in our suburban locations and strong off-premises digital sales across all markets. For our fiscal year to date through September 26, 2021, we experienced positive momentum across all of our channels, as COVID-19 vaccines became widely available and customers started to return to offices.

Sweetgreen has consistently expanded during its life, noting in the same filing that it had “119 restaurants as of the end of fiscal year 2020,” and 140 as of the end of September of this year. That growth has not been inexpensive, with Sweetgreen “targeting” an “average investment of approximately $1.2 million per new restaurant” in the future.

Powering Sweetgreen in the background are a few trends that the company views as accretive, including a consumer shift toward more plant-based eating and “rapid adoption of digital and delivery,” key channels for the food chain’s revenue growth.

Regardless of how you feel about Sweetgreen the brand, the company’s overall business plan appears sound on paper. People are eating healthier and ordering more via delivery. Salads transport well — they are not soup — and are as plant-based as you’d like. And because it is possible to make money selling food, why not Sweetgreen?

So, how has the company managed in business terms during its last few years of growth? Let’s take a look.

Does Sweetgreen’s business generate sweet amounts of green?

No, it does not.

In fact, Sweetgreen is rather unprofitable and doesn’t appear to be on the cusp of a rapid march toward profitability. Not that losing money is a sin, per se; many venture-backed companies run stiff deficits while they scale. That is the point of raising private capital, to invest it at the cost of near-term profitability and cash flow.

But Sweetgreen is no corporate child. It was founded in 2007, per Crunchbase data, making it nearly old enough to secure a learner’s permit to drive in the United States. If a human can get to the point of nigh-maturity in a time frame, surely corporations made up of adults and backed by mountains of private capital can manage the same?

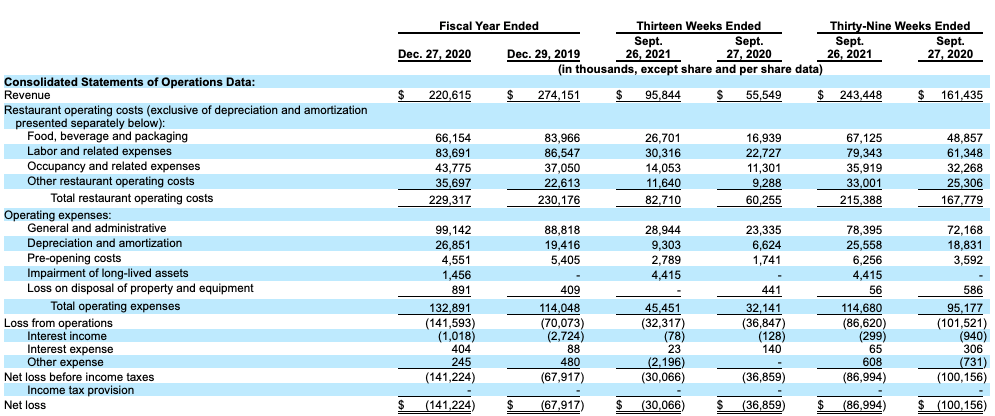

Here’s the data:

Note that time flows east to west on this particular table, so the company’s most recent full fiscal year is on the far left.

As we can see from the two most recent fiscal years, 2020 was a pretty hard time for Sweetgreen, which saw its revenues decline from $274.2 million to $220.6 million, and its net losses double from $67.9 million to $141.2 million over the same time frame.

More recently, the company has returned to growth. In the three quarters concluding in late September, for example, Sweetgreen managed to post $243.4 million in revenue, far ahead of its $161.4 million tally from the year-ago period. Over that time frame, however, losses proved very sticky, only falling from $100.2 million (2020 through September 27) to $87.0 million (2021 through September 26).

Most recently, comparing the quarters ended in late September 2020 and 2021 — the middle pair of columns in the above table — the company’s revenue grew mightily from $55.5 million to $95.8 million. But in contrast, the company’s net losses only declined from $36.9 million to $30.1 million over the same period.

What we are not seeing, then, is the sort of operating leverage we like to observe in companies that are posting rapid growth. As Sweetgreen’s revenues expand, in other words, its losses don’t seem to evaporate as rapidly. That’s not great.

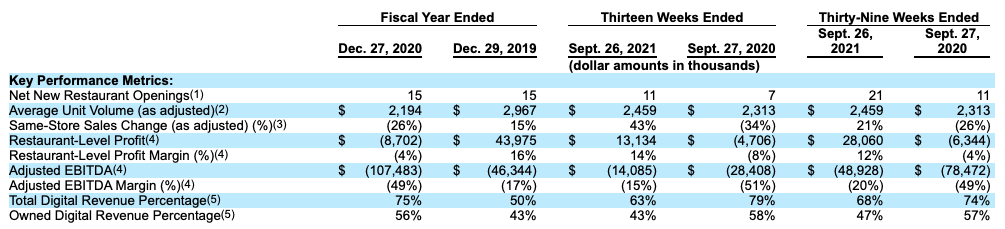

Past the above wall of GAAP metrics, the company makes its pitch through the lens of a host of metrics that are non-GAAP, but still interesting. Observe:

These are the same time periods as before, in case that helps with your reading.

Fans of non-GAAP profit metrics like adjusted EBITDA will note that the company’s adjusted profit margins have improved year over year in both the 39 weeks ending in late September 2021 and in the most recent 13-week period — roughly one quarter. Yes, they have, but the company remains far from profitable thanks to its corporate costs.

Notably, the company removes “depreciation and amortization” costs from its adjusted EBITDA metrics, a decision that we’ll get back to shortly.

You’ll note in the above chart that the company presents two “restaurant-level” profit metrics. This method of presenting corporate results is a way to disaggregate the profitability of Sweetgreen’s actual restaurants from its corporate costs; if the company generates enough profit from its actual restaurants, it will be able to cover its overall cost structure.

In the 13 weeks concluding September 26, 2021 “restaurant-level” profit was $13.1 million. Here’s how the company defines that metric:

We define Restaurant-Level Profit as income (loss) from operations adjusted to exclude general and administrative expense, depreciation and amortization, pre-opening costs, impairment of long-lived assets, and loss on disposal of property and equipment. Restaurant-Level Profit Margin is Restaurant-Level Profit as a percentage of revenue.

To which we have to reply, wait a minute. Why aren’t “depreciation and amortization” presented as restaurant-level costs that would impact restaurant-level profits? I think because they would cut the company’s most recent 13-week “restaurant-level” profit from $13.1 million to $3.8 million. Which would make the company’s same-quarter $36.1 million in other non-restaurant-level operating costs appear pretty damn high.

In our view, they should be included in restaurant-level results because they stem from opening and running restaurants.

Discussing the 13-week period ending September 26, 2021, the company shares the following regarding its $9.3 million worth of depreciation and amortization costs, worth some 10% of revenues:

The increase in depreciation and amortization for the thirteen weeks ended September 26, 2021 was primarily due to the 32 Net New Restaurant Openings during or subsequent to the thirteen weeks ended September 27, 2020, and an increase of internally developed software to support our digital growth.

Unless we’re misunderstanding how the company deals with depreciation and amortization costs, it appears that the company’s actual business of operating restaurants and selling food is not that great in terms of generating profits that can be used to pay for its larger corporate efforts. And I don’t think that we are.

Including depreciation and amortization costs in both adjusted EBITDA and “restaurant-level” results would make each appear far worse, but would also be fairer. This feels a bit akin to how Rent the Runway wants to obfuscate its clothing depreciation costs in certain profit metrics. We’re not sold on how Sweetgreen is handling its own numbers.

We could continue for ages, as this S-1 is incredibly interesting. But let’s work toward wrapping with some notes on cash flow and a look to the future:

Recall that free cash flow is operating cash flow minus investing cash flow. As we can see in the above, Sweetgreen is incredibly cash-hungry on both counts, leading the firm to post very negative cash flows in each fiscal year and partial fiscal year discussed above. Not great!

To its credit, the firm appears to understand that its current model isn’t sufficiently profitable at the restaurant level to finance its overall cost structure, so it’s investing in lowering its labor costs. As Sweetgreen writes (emphasis: TechCrunch):

In September 2021, we completed the acquisition of Spyce Food Co. (“Spyce”), a Boston-based restaurant company powered by automation technology. The purpose of the acquisition is to serve our food with even better quality, consistency, and efficiency in our restaurants via automation. This investment has the potential to allow us to elevate our team member experience, provide a more consistent customer experience, and, over time, improve our capacity and throughput, which we believe will have a positive impact on Restaurant-Level Profit Margin.

If that works, hell yeah. Robot salads. Bring them the fuck on. I will eat them. But how long “over time” will prove to be is not clear.

Finally, Sweetgreen has two classes of shares — Class B, with 10 votes, and Class A, which have but one. That a salad company is following the Silicon Valley trend of giving insiders incredibly powerful voting power to ensure outsize corporate control is funny. The argument in favor of conserving voting power in the hands of, say, founders, is that it will allow them to make hard choices that are good for the business in the long term; things like big bets on new technology.

Recall that Sweetgreen makes and sells salads.

What’s the company worth? We have no idea. It was last valued somewhere between $1 billion and $2 billion on the private markets. Let’s see.

Comment