Welcome back to the week, and welcome back to The Exchange. Robinhood has yet to file its IPO, so we’re looking at other companies in the meantime. Today it’s Babylon Health, a British health tech company that is pursuing a U.S. listing via a blank-check company, or SPAC.

You have questions. I have questions. We’ll get to some answers.

But before we do, we wanted to note that Anna and I are looking into the AI startup market tomorrow morning. If you are a VC with notes regarding the current pace of investment into the sector or thoughts on where customer traction is highest, let us know. If you are a founder building an AI-powered startup, we’d also like to hear from you about what you are seeing. Use the subject line “AI startups,” please.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

With that out of the way, let’s get into Babylon Health. We’ll kick off with a short riff on its fundraising history, talk about its product, and then dive into its numbers and, bracing ourselves for impact, its projections.

The larger context this morning is that we’re doing legwork ahead of what could be a super active Q3 2021 IPO cycle. Kanzhun, a Chinese company, has also filed for a U.S. listing. Toss in Robinhood whenever it gets off its duff and gives us its own filing, and we’re being promised a good time.

Babylon Health

Per Crunchbase data, Babylon has raised north of $600 million as a private company. Its funding, however, has not come from sources that we tend to discuss here at TechCrunch. Instead, the company raised some money from more traditional investors like Hoxton Ventures and Kinnevik, but the bulk of its capital was raised from the Saudi Arabian “Public Investment Fund,” or PIF. The PIF led a $550 million round into the British health tech company back in August 2019.

PitchBook has the round cut into two parts, the larger, first portion of which valued the company at $1.9 billion on a post-money basis.

That figure brings us to the SPAC deal that Babylon is now pursuing. The company’s new equity value after its SPAC deal will land around $4.2 billion, with Babylon sitting on around $540 million in cash after the deal is completed. The company will sport a lower, $3.6 billion enterprise valuation after its merger with SPAC Alkuri.

So, it was a unicorn pre-SPAC. And it’s going to be an even bigger unicorn after the deal is completed. What did it build to attract so much money? Great question!

What does it do?

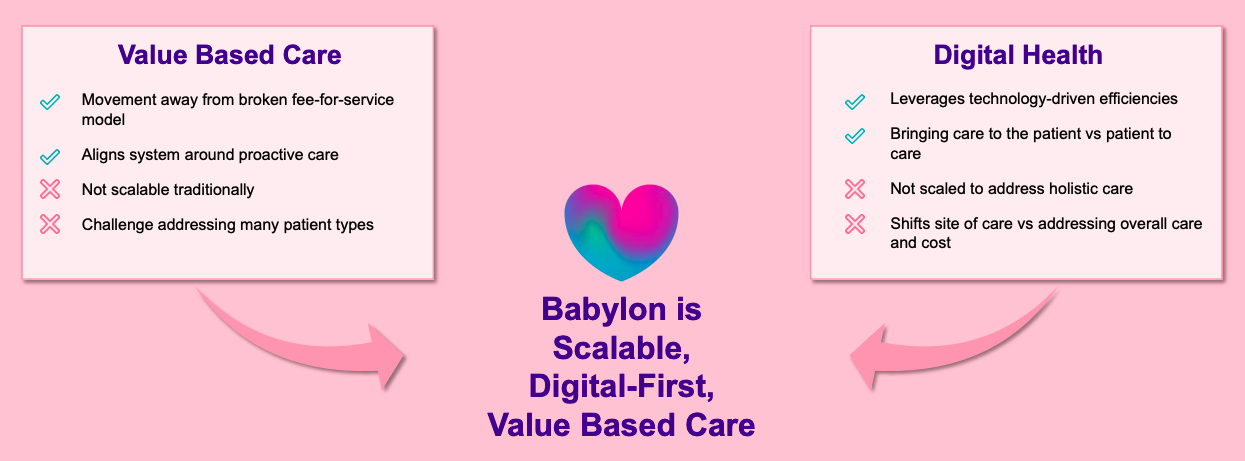

The core thesis of Babylon, as far as we can tell, is that the global healthcare market is pretty broken and that a combination of digital services, AI and preemptive care can help improve it.

In more specific terms, Babylon likes to call itself a provider of “Digital-First Value Based Care.” We’d amend that to digital-first, value-based care (VBC). The first term is somewhat obvious. The latter less so.

Babylon defines VBC as an “arrangement where providers are paid the total health budget for the managed lives.” And at the union of both digital services and VBC sits the company, hopefully solving the weaknesses of each concept by letting them support one another.

For fun, here’s how the company makes that part of its pitch to investors:

Image Credits: Babylon deck

The company executes that model in three revenue-generating ways. The first is its software, which it licenses to other companies. The Babylon software package helps assist end customers with health assessments, triage and monitoring their care and is sold on a contract basis.

Babylon also offers what it calls “virtual care,” which we can probably think of as telehealth services. And, finally, the company offers the aforementioned VBC, in which Babylon gets its customers the IRL care and rehab that they need.

How does the model improve health systems that are famously expensive, hidebound and generally shit? By swapping in low-cost telehealth for ER and in-office doctor visits, for one. And by providing preventative care to try and avoid more costly health appointments.

The company’s software fees are sold on an annual basis to other companies. Its virtual services are paid for by a fee-for-service model, and its larger VBC model is somewhat akin to insurance in that it takes in regular fees and covers “all costs incurred in both primary, secondary and tertiary care settings, with stop-loss protection.”

Babylon expects to generate around 85% of its revenues in the U.S. market for the foreseeable future (based on 2021 and 2023 estimates, and directional change in anticipated market share), with software incomes making up around a 10th of its revenues over the same time frame.

Taking all that in hand, we can now dig into Babylon’s historical numbers and its projections.

Results

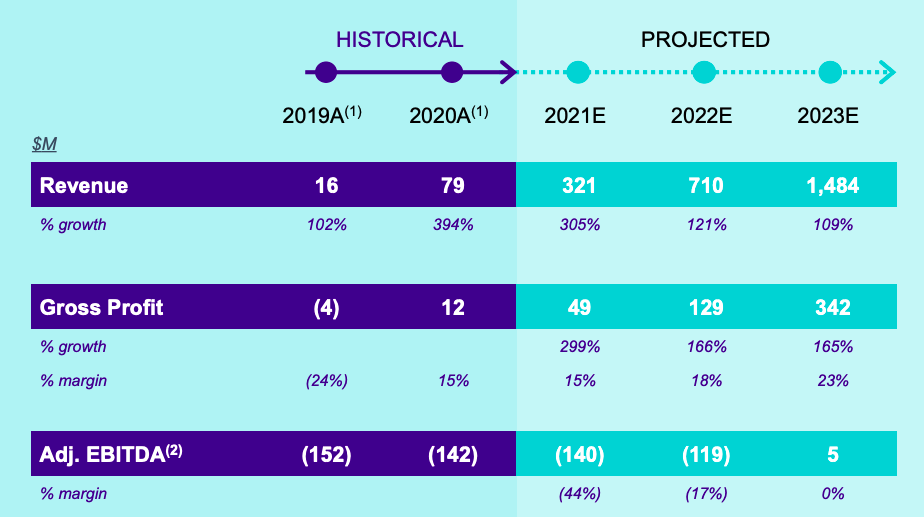

Don’t get mad at me for the following graphic. I did not design it.

Image Credits: Babylon deck

Babylon had revenues of $16 million in 2019 and $79 million in 2020. The resulting growth rate of 394% is more than good.

Looking into the future, Babylon expects its revenue growth to slow, while the pace at which it adds revenue to rise; the larger base from which the company will measure future growth rises, making its future top-line accretion more impressive in dollar terms than when measured as year-over-year percentage growth.

The company’s adjusted EBITDA line item is pretty whatever. I read the historical and projected figures as saying, “We’ve lost money, we lose money, and we will keep losing money for some time.” The adjusted EBITDA breakeven point in 2023 is ambitious.

Numbers that we trust a bit more can be found in the gross profit section of the chart. Critically, Babylon managed to pull its model from gross margin negativity into gross margin positivity in 2020. That’s huge. It would be far harder for Babylon to SPAC at the price it wants if it had not shown that its business could generate not only gross margin improvements, but that it can actually generate gross profit as it scales.

(Gross) operating leverage! Woo.

Notably, Babylon doesn’t expect gross margin improvement in 2021, even if its gross profit will rise as it holds a 15% gross rate against rising revenues. As the future unspools, the company does anticipate gross margin improvements to complement its revenue gains. That’s good, if far off.

In closing, Babylon is a very complex company with a multipart business model, revenue streams of varying quality, a diversified geographic footprint and more. And frankly, despite its SPAC deck, I still want more from the company. Like a full, standard S-1 filing. It’s weird that SPACs are able to put together such huge deals while only hitting on select questions.

But then again, what are private investors up to? The same.